By Jake Liddle

At the beginning of this year, China’s National Health and Family Planning Commission, along with seven other ministries, issued a new policy designed to streamline pharmaceutical distribution channels. The policy, which regulators are piloting in a number of provinces before an expected countrywide reform in 2018, will change the way manufactures, distributors, sales, and compliance teams in the pharma industry operate from both a business and tax perspective.

The policy introduces a ‘two invoice system’, meaning that during the distribution process from drug manufacturer to hospital, only two tax invoices, or fapiao, may be issued. This aims to both reduce the cost of pharmaceuticals and to prevent corruption.

As of yet, the policy is being piloted in the regions of Anhui, Jiangsu, Fujian, Qinghai, Shanghai, Zhejiang, Hunan, Chongqing, Sichuan, Shanxi, and Ningxia.

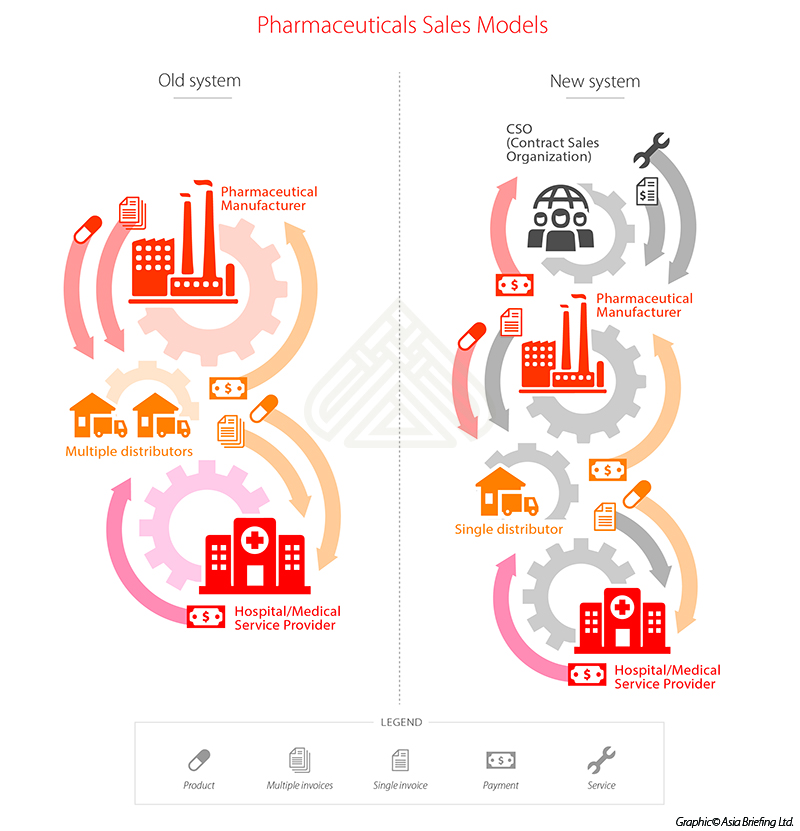

The two invoice system for the pharmaceutical industry

According to the new system, the manufacturer issues a first invoice to the distributor, while the distributor issues a second invoice to the hospital or medical service provider.

Previous distribution chains were typically comprised of manufacturers who sold to multiple distributors at relatively low prices. The distributors would sell the products to hospitals at a higher price, while high profit margins would fund sales and marketing expenses. The two models are presented below:

The new two invoice system leaves manufacturers with the autonomy to directly procure their pharmaceutical products, or delegate the logistical process to a single provider, allowing only one commissioned distributor in the procurement chain. The two-invoice system will decrease the retail price of pharmaceutical products for the medical service provider, and improve transparency within the distribution chain.

However, in some cases, especially in more rural areas, where the distributor is not able to operate, a distributor may use a third party to complete product deliveries with authorization from the provincial-level pharmaceutical procurement administration.

The new model will implicate contract sales organizations (CSOs), which serve as a means to replace commission or service fee arrangements, and will act as sales and promotional operators for manufacturers.

Impact on pharmaceutical business models

The two invoice system will have impact on the way in which pharmaceutical companies operate from both a business and tax perspective.

The two invoice system will mean that distribution channels of pharmaceutical products will change from a hierarchical structure to a flat one. Further, pharmaceutical companies may have to change distributors.

This is particularly pertinent in more rural areas, where companies will need to directly negotiate with local distributors. Consequently, smaller distributors will eventually be bought out and forced out of business, as the system will call for a more unified distribution network.

The two invoice system also means that hospitals are able to confirm the batch number of the pharmaceutical products they receive from the manufacturer or importer, as well as the exact ex-factory price.

As the disparity in pricing between the hospital purchase price and manufacturer’s ex-factory price is much greater in the two invoice system, manufacturers will have to ascertain what their ex-factory pricing scheme is:

- If manufacturers decide to increase the ex-factory price to match the purchase price, excluding distribution fees, this may affect the retail price, resulting in a higher VAT payable by the manufacturer.

- If manufacturers decide not to increase the ex-factory price, the pricing information will be made available for hospitals to review, possibly resulting in demands for lower sales prices.

While this latter development is a positive for buyers, this may affect manufacturer’s profits, as they will need to consider the fees paid to CSOs under the new structure.

![]() RELATED: Business Advisory Services from Dezan Shira & Associates

RELATED: Business Advisory Services from Dezan Shira & Associates

Compensation paid to CSOs will depend on the nature of their scope and operation. Commission-based pricing may apply if CSOs operate as multi-layer distributors, but an added cost arrangement may suffice if CSOs provide more supportive roles to manufacturers.

How to prepare your business

Under the new system, distributors that used to operate under the alongside multiple other distributors on a second or third-tier level in a hierarchical structure, will become primary distributors, and manufacturers will have to directly engage with them.

To achieve these goals, however, companies engaged in the industry – manufacturers, distributors, and buyers – need to conduct due diligence to ensure their business partners are capable and compliant operators. Further, businesses across the supply chain need to ensure their staff – including sales, marketing, and procurement teams – are briefed on the two-invoice system and its impact on their job roles.

Distributors for the industry will now be exposed to greater scrutiny from both regulators and business partners. This will help distribution channels to operate in more transparent way in line with international best practices, and international businesses maintain compliance with Bribery Act and Foreign Corrupt Practices Act (FCPA) compliance.

It is important for pharmaceutical companies’ legal and marketing teams to keep abreast of the healthcare reform and the two invoice system. They should assess and adjust business models according to the changes made by the policy, which may involve engaging CSOs. Preemptive measures to absorb tax implications relating to transfer pricing and promotional activities, such as pricing adjustments regarding ex-factory prices, and revisiting existing arrangements with e-distributors should be made. This may be done by observing the methods of operation now utilized in Sanming city in Anhui province that had initiated the reform in 2011, and has since successfully implemented the system.

This article was first published on China Briefing.

Since its establishment in 1992, Dezan Shira & Associates has been guiding foreign clients through Asia’s complex regulatory environment and assisting them with all aspects of legal, accounting, tax, internal control, HR, payroll, and audit matters. As a full-service consultancy with operational offices across China, Hong Kong, India, and ASEAN, we are your reliable partner for business expansion in this region and beyond.

For inquiries, please email us at